Summer 2024

A recent survey found that 59% of workers thought that they were contributing to their 401(k) plan and saving for retirement when they weren’t.

The Retirement Security Survey, conducted by Principal, asked participants why they weren’t enrolled in the plan and a surprising number thought they were. Even though plan provisions such as automatic enrollment and employer matching have a positive effect on plan participation, communication can also be a powerful tool.

The Department of Labor (DOL) and Internal Revenue Service(IRS) require a variety of information be shared with plan participants, but some eligible employees can be intimidated by the language in the material and decide that participation is too complicated. Others believe they are automatically enrolled in the plan because they were auto enrolled at a past employer.

If possible, one-on-one meetings are a great way to make sure that an employee understands what is being offered. When an employee is hired, they may receive an email with multiple files attached, including instructions to log onto a website and enroll in the 401(k). Starting a new job is often overwhelming and enrollment can be overlooked.

Enrollment meetings involving both Human Resources and the plan’s investment advisor are a great way to boost communication and participation. Taking the mystery out of available investment options, as well as showing the financial benefits of saving for retirement, helps the participants feel confident in their choices. Enrollment meetings can be done in person or by video meeting, depending on the location of the employees.

If it’s available to you, a retirement readiness report will show each participant their retirement age, current balance, current deferral percentage, current income and what retirement will look like for them. It can be quite an eye-opener for many participants.

Communication is the key to successful plan participation. It also helps your participants have a more positive attitude toward your retirement plan and their retirement future. Feeling like their employer cares about their future leads to a higher level of job satisfaction and feeling appreciated.

Participant Notices: A Quick Overview

Participant Fee Disclosure:

- Pertains to participant-directed accounts.

- Provides certain plan information as well as fees that may apply.

Investment Comparative Chart:

- Pertains to participant-directed accounts.

- Provides plan investment information such as past performance, expense ratio, and fees.

Automatic Enrollment Notice:

- Pertains to 401(k) plans that include automatic enrollment provisions.

- Provides the default deferral rate that will apply unless they make a different deferral election and the instruction for how to do so.

Safe Harbor Notice:

- Pertains to plans with Safe Harbor contribution provisions.

- Provides information about contribution and vesting provisions.

Qualified Default Investment Alternative (QDIA) Notice:

- Pertains to plans that allow for participant direction and utilize a qualified default investment for those participants who don’t make an election.

- Provides information about the investment option that will be used for their contributions if they do not make an investment election.

Universal Availability Notice:

- Pertains only to 403(b) Plans.

- Provides information regarding the opportunity to contribute to the 403(b) Plan.

Summary Plan Description (SPD):

- This is a simplified version of the plan document provisions which needs to be provided within 90 days of when the employee becomes eligible for the plan.

- Updated copies must be provided every 5 years if there are changes to the plan. Every 10 years if no changes are made.

Summary Annual Report (SAR):

- Summarizes the plan information on Form 5500 for the participants, such as total plan contributions, distributions, fees, plan asset balance, and participant count.

- Distributed within 2 months after the Form 5500 filing deadline, including extensions.

Annual Funding Notice (AFN):

- Pertains to defined benefit plans, including cash balance plans, that are covered by the Pension Benefits Guaranty Corporation (PBGC).

- Due 120 days after the close of the plan year for large plans and the earliest of the day that the Form 5500 or the date that it’s due, including extensions, for small plans.

Summary of Material Modifications (SMM):

- Provides information regarding changes made to plan provisions by a plan amendment.

- Due no later than 210 days after the close of the plan year for which the modification was adopted.

Mastering the Art of Distributing Participant Notices

Define your roles and responsibilities

Defining roles and responsibilities within your plan administration is akin to establishing an Investment Policy Statement for financial decisions. A well-documented communication policy specifies who manages notice distribution, verifies receipt, handles undeliverable notices, and outlines procedures for both active and terminated employees.

Clarify who will receive communication

Before distributing notices, it is crucial to identify the recipients. This includes:

- Active employees who are eligible and participating – these are employees who are currently employed and who are contributing to the plan. These employees are required to receive all relevant regulatory notices.

- Terminated employees with a balance in the plan – these are still participants in the plan, even though they are not actively employed. As long as they have assets in the plan, they are required to receive all relevant plan communication. NOTE – these are some of the hardest individuals with which to maintain communication, and therefore require extra effort.

- Active employees who have a balance in the plan but are not actively contributing – these are employees who are currently employed who have either elected not to contribute to the plan or who may be on leave. These employees, with assets in the plan, must still receive all relevant plan notices.

- Active employees who are eligible for the plan, but do not have a balance and who are not contributing to the plan – these employees require a decision from the Plan Sponsor. While providing them with all plan information is never wrong, the Secure Act 2.0 allows for these employees to receive a one time of year Eligibility Notice. The notice serves as a reminder of their opportunity to participate in the plan and their rights to request any or all plan information, but states that until they are participating in the benefit, they will not receive any information from outside of the Eligibility Notice.

- Active employees who are not eligible for the plan — these are employees who are actively employed but have not met the terms of the plan document to become eligible for benefits. These employees are not required to receive any plan communication until they fall within the plan window for eligibility or enrollment.

Define how notices should be distributed

How participant notices are required to be distributed has evolved over time based on requirements by the DOL and IRS. Both first class mail and electronic mail are available, but they have procedures that must be followed.

First Class Mail – The address provided by the participant within the retirement plan benefit system is used for this mailing unless you are aware that the delivery address on file is not current and/or if the participant has notified you (in writing is best) to utilize a different address.

Electronic Delivery – There are two segments of the“eDelivery” rules for participant notice distribution:

Wired at work – for participants who provide a work email address, who are actively employed, and who have access to needed equipment to utilize this email address, the Plan Sponsor is allowed to distribute all notices to this email address. However, a system should be developed on how to provide notices to them after they are no longer active with the company to ensure that their work email is not their plan level contact.

Personal email – to distribute notices to a personal email address, a paper notice must first be distributed to the participant declaring that future notices will be distributed electronically. This paper notice must provide the participant with (1) confirmation of the personal email address that will be used, (2) how the participant can request use of a different email address, (3) the participant’s right to opt out of electronic notice delivery, and (4) the proper plan contact for any questions regarding the plan. After this paper notice has been distributed, future notices can be sent to the identified email address.

How to address undeliverable notices

After notices have been distributed, it is important to address any notices that were undeliverable. For notices sent by first class mail, this includes mail that was “returned to sender”. For electronic mail, these are emails that “bounced back”. For any notice that is returned undeliverable, there should be a process in which a better address is identified and the notice is resent. It is also best to confirm if the new address provided is the best ongoing address for future communication or just a temporary contact. It is very important to confirm that each notice is being received by all participants in your retirement plan. Special attention should be paid to terminated employees with a balance in the plan. These employees have the highest risk of being considered “missing”. Missing participants have been a focal point of the Department of Labor and their plan level audits; therefore, confirming that the plan has good contact information for these participants could prevent the plan the distraction and costs of a plan investigation.

Missing participants

Addressing missing participants is critical to compliance and plan integrity. The DOL’s Employee Benefits Security Administration(EBSA) has outlined Best Practices that the plan should follow regarding communication and location processes for these missing participants:

- Maintain accurate census information for the plan’s participant population

- Implement effective communication strategies

- Attempt missing participant searches

- Document procedures and actions

These suggested practices are explained in more detail on the EBSA website.

Conclusion

Understanding and adhering to notice responsibilities is fundamental for plan sponsors to mitigate risks and ensure regulatory compliance. By defining roles, clarifying recipients, establishing clear distribution methods, and addressing undeliverable notices promptly, sponsors can effectively manage their retirement plans. Remember, diligent tracking and technological tools are essential in confirming receipt and maintaining communication with all participants.

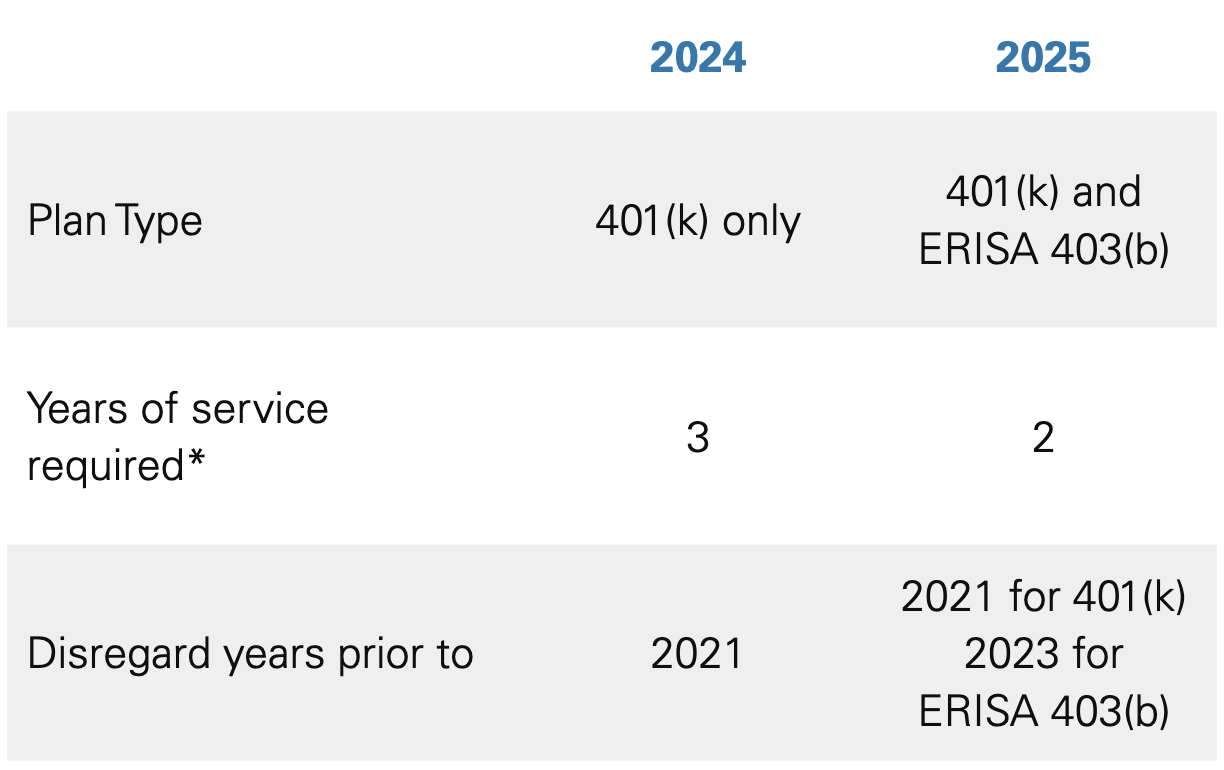

Plan Ahead for 2025 Long-Term, Part-Time (LTPT) Employees

As a reminder, eligibility requirements went into effect for Long-Term, Part-Time (LTPT) employees as of January 1, 2024. However, additional changes that affect who is considered a LTPT employee will be coming for 2025. Please see the chart below to plan ahead and ask us if you have any doubts!

*minimum 500 hours/year over consecutive years

This newsletter is intended to provide general information on matters of interest in the area of qualified retirement plans and is distributed with the understanding that the publisher and distributor are not rendering legal, tax or other professional advice. Readers should not act or rely on any information in this newsletter without first seeking the advice of an independent tax advisor such as an attorney or CPA.

© 2024 Benefit Insights, LLC. All Rights Reserved.